What follows below is a transcript of my interview earlier this morning with Senator John McCain on the investor class and the stock market. Big Mac is talking tax cuts on capital gains, businesses, and individuals. There is no question that he is energized. Politically, he is still running even with Obama among investors. That is not good. Is there time for Senator McCain to break through and run up his margin with this crucial voting block?

Larry Kudlow: Let me go back to the first question, which you were beginning to answer. We've had this terrible stock market slump. Some say $3 trillion dollars worth of wealth have been lost by investors in the investor class. And I was asking, and I think you were answering, what is your plan to create some recovery in the stock market?

Senator McCain: Keep taxes low, cut spending, create jobs with alternative energy, including nuclear power plants, including drilling offshore, wind, tide, solar. Free us from our sending $700 billion or whatever it is across to countries that don't like us very much.

Free up credit. Larry, I’ve been meeting with a lot of small businesspeople, and they're having great difficulty getting lines of credit. This is something we've got to free up. Now, we have given the banking, the banks and other institutions the kind of infusion they need. It's time they pass that on to small businesses who say they can hire. They've got business, but they just haven't got the line of credit.

But make sure that everybody knows that we're going to keep taxes low. We're not going to raise taxes. We're the creator of business and the engine of our economy and small business, Senator Obama's proposal would tax half of all small business income, some 16 million jobs in America would be at risk. And then you put on top of that, he will force his mandated health care plan on small businesses, their employees, and their children. It's not good for America.

Kudlow: Just on the credit piece that you mentioned a few moments ago, have you and your campaign been following the improvement in the Libor credit market in London and the commercial credit markets here in New York? It looks like the Treasury plan is beginning to work. That may be a positive sign. Do you follow those areas?

McCain: Yeah, I do, and I get updates all the time. One of the areas that I’m still very disappointed in, though, Larry, and you may not agree with me, we've got to go in and get these home mortgages bought and give people mortgages they can afford so they can stay in their home. Look, I’m in Ohio. Homes are being foreclosed everywhere. A lot of these people, it's their primary residence, could stay in their home if they had a new mortgage at the new value of their home, at payment levels they could afford. That is the slow -- one of the slowest parts. I think it's the slowest part right now. Keep people in their homes. If they can't realize the American dream and stay in their homes, then obviously, the rest of this equation is hard to complete.

Kudlow: Let me swing back to the investor side. There are about 100 million investors, according to the Federal Reserve survey. And interestingly, in recent national elections, they're a huge voting block, almost two of every three votes cast are cast by people that own stocks either directly or indirectly. And yet, sir, you very, very seldom mention investors on the campaign trail. Why is this?

McCain: Well, I try to talk about them more often. A lot of the people that come, frankly, are people that are having trouble staying in their homes, keeping their jobs, et cetera. But I think it goes back to all this business of Senator Obama's view of "fairness." When Charlie Gibson said, why would you want to raise capital gains taxes when you know it will decrease revenue? And he said in “fairness”. And he told Joe the Plumber -- Joe the Plumber got the message through better, what we've been trying to do this whole campaign. [Obama] wants to "spread the wealth around." That takes from the investor class. That takes money from one group of Americans and gives it to another. Now that signal has been very clear. And I think people ought to pay attention to it, because it's been tried before in other countries, and policies of other left, liberal administrations. It doesn't work, and it's bad for America. We want to encourage the investor class, and that means capital gains and dividend taxes are low.

Kudlow: You've just unveiled a new tax cut on capital gains. Can you tell us about that? Because in some sense, that's probably the most important investor class tax.

McCain: It's the most important in many respects, Larry, and we want it low and we want it lowered. Every time -- there's one tax that there's no argument about, that every time it's been lowered since Jack Kennedy, we have seen an increase in revenues. Now, why anybody would argue, as Senator Obama does, that we need to raise it, even if it's -- of course, the amount needed to raise it is varied with whatever poll he's taken, but the point is that we want to lower it and keep it low and encourage investment, especially now in America in these difficult times.

Kudlow: But Senator, what is -- the current law rate is 15%.

McCain: Yeah, yeah.

Kudlow: You're taking the cap gains rate down to what?

McCain: First down to 10%, I would like to see it, and gradually even make it lower. Look, why should we tax people's gains twice? Why should we tax them twice, okay? They make an investment, they should be able to get their returns on their investment. And capital gains is obviously -- low capital gains tax is probably the greatest incentive for investment that we have in America today. And so, look, I’ll be glad to listen to smart people like you, Larry, but the worst thing we can do is tell people we're going to raise it, and that, obviously, would chill investment in America, right?

Kudlow: Well, with your lower capital gains tax, which in a recent speech you said 7.5% for two years, are you surprised, though, that respected pollsters like Scott Rasmussen or Investors Business Daily are still showing you running neck and neck, even with Mr. Obama? Back in 2004, President Bush beat John Kerry by 11 percentage points among investors. Now, you've got a lower cap gains tax. Mr. Obama proposes to raise the cap gains tax from 15% to 20%. Except you're still running even in the polls. Can a Republican win running even among investors? And why don't you think your message on capital gains has resonated with a bigger margin among investors?

McCain: I'm not sure, except obviously, when he broke his word that he would take public financing if I also did, he signed a piece of paper, that obviously, he's had a huge money investment. Look, I’m a 7.5%, I’d like to keep it permanently at 7.5%. Right now, we need more investment in America and in the stock market and in businesses and investment than ever before in these difficult times. So, it's pretty clear that if we keep them low, we will provide another tool for encouraging investment. Look, we are -- I am so happy we are where we are. I see a level of enthusiasm out here in this campaign, Larry that is remarkable. I haven't seen this level of enthusiasm before. I'm very optimistic, and we're coming from behind. I'm the underdog. That's where we always like to be. But we are within margin, and I’m very happy where we are.

Kudlow: Another really important tax for the stock market investors, of course, is corporate profits. Profits are the mother's milk of stocks, as I have said from time to time. You've proposed to lower that from 35% to 25%. Senator Obama says the other day, that's merely another huge and permanent tax cut for corporations, including $4 billion dollars for the big oil companies, but it is no help for workers. Would you react to Mr. Obama's criticism of your corporate tax cut?

McCain: He doesn't get it. Corporate tax rates in America are the second highest in the world. Japan is only higher. Ireland has 11%. Business -- I like to call them business taxes, because that's what they really are, because they're businesses and they create jobs and they create employment. And when businesses can go anyplace in the world, where are they going to go? Look, I can name you Fred Smith of FedEx, Meg Whitman, other CEOs who will tell you, when they have a choice to go around the world and pay less in taxes where they can invest more and increase businesses and jobs, they're going to do that. Obviously, they want to stay in America. And they want to create jobs in America, and they will, but we want to give them the incentive to do so. And lowering the business tax, the corporate taxes, in my view, they should be lower than 25%. Why is it that we're the second highest in the world, when 20 or 30 years ago, we were amongst the lowest in the world? It's not an incentive to businesses and jobs in America. It shows, frankly, that Senator Obama just doesn't get it.

Kudlow: You said yesterday or the day before when you were in Miami, Florida, the Democratic Congress is going to remove tax incentives or tax preferences for 401(k) accounts. Of course, that is a huge investor issue. What did you mean by that? What is the plan that Democrats want to take away from 401(k)s?

McCain: Well, that's exactly what they're saying. And Barney Frank, who is powerful, chairman of a powerful committee in the House, said we're going to raise taxes and we're going to increase spending. That's exactly the wrong thing to do in the economic difficulties we have. How did we get into this ditch? We ran up a $10 trillion deficit on our kids and half a billion dollar debt to China. So, obviously, they want to take the 401(k)s and use that money to give that to the government to spend, rather than people, and I think that's very dangerous disincentives to savings, which is exactly the cause of one of our problems, as we all know.

Kudlow: Last one, Senator, and I appreciate your time very much. Americans have an innate sense of optimism and confidence about stocks and the economy. The Rasmussen poll shows 73% believe stocks will be much higher five years from now than they are today. Is there a way for you in the closing days of this campaign to appeal to the innate sense of optimism that Americans have? Is there a way for you to connect with the investor class?

McCain: Well, I hope we've connected with the investor class by them examining our plans as we come closer to the election. But I also have to tell you, Larry, the people who want to invest are Joe the Plumbers of this world who want to own their small business. They want to employ people, and they want to invest in their futures and in the stock market and make investments, 401(k)s, IRAs and others, so that they could ensure their retirement and their future. And Joe the Plumber was able to do something that we hadn't been able to do this whole campaign, and that is articulate the reason why he doesn't want to see his taxes raised so that he can use it to buy a business and create jobs and to take care of his and his family's future. That's what this campaign is boiling down to, and that's why we're getting closer and closer, my friend.

Kudlow: All right, Senator McCain, thank you ever so much for sharing your time. Good luck in the rest of the campaign, sir.

Friday, October 31, 2008

The Dumbest Story Ever Told

Today’s GDP report showed a small contraction of 0.3 percent. But stocks went up nearly 200 points anyway. Many observers believe the thirdquarter downturn was not a catastrophe, especially if you factor in hurricanes and the Boeing strike. On top of that the short-term tax rebates ran out in the third quarter, and that helped depress consumer spending, which did fall 3.1 percent.

However, inventories are quite low after three quarterly declines. And business capex shipments actually rose slightly in the three-month period ending in September. So there’s no collapse, at least yet, in business investment.

Most analysts expect a much worse drop in the fourth quarter, ranging between a 3 and 4 percent contraction. But they are not factoring in a roughly $200 billion annual drop in consumer energy expenses that will accrue from the collapse of oil and gasoline prices. This is going to be a big consumer booster.

Meanwhile, credit markets continue to defrost and commercial paper is now rising again, as is inter-bank lending. So the economic story may not be near as bad as the consensus thinks. Remember, of course, the Fed is pumping in cash at a huge rate. That’s going to help the whole story.

The dumbest thing I heard today on the economy was a statement from Sen. Obama. He says the decline in GDP is “a direct result of the Bush administration’s trickle down, Wall Street first, Main Street last policies that John McCain has embraced for the last eight years and plans to continue for the next four.”

Wait a minute. Did I miss something here? After the bursting of the tech bubble and the 9/11 attacks, George Bush lowered tax rates across-theboard for individuals and investors. The stock market rallied uninterruptedly for five years. The economy expanded from the end of 2001 to the end of 2007. Are we to really believe the Obama narrative that cutting tax rates is the cause of this downturn? Not the credit shock? Not the Obama-supported government mandate to sell unaffordable homes to low-income people and to pressure Fannie and Freddie to securitize these loans? And not the oil shock, as well?

It was really tax cuts that caused this recession?

That’s the dumbest story ever told.

However, inventories are quite low after three quarterly declines. And business capex shipments actually rose slightly in the three-month period ending in September. So there’s no collapse, at least yet, in business investment.

Most analysts expect a much worse drop in the fourth quarter, ranging between a 3 and 4 percent contraction. But they are not factoring in a roughly $200 billion annual drop in consumer energy expenses that will accrue from the collapse of oil and gasoline prices. This is going to be a big consumer booster.

Meanwhile, credit markets continue to defrost and commercial paper is now rising again, as is inter-bank lending. So the economic story may not be near as bad as the consensus thinks. Remember, of course, the Fed is pumping in cash at a huge rate. That’s going to help the whole story.

The dumbest thing I heard today on the economy was a statement from Sen. Obama. He says the decline in GDP is “a direct result of the Bush administration’s trickle down, Wall Street first, Main Street last policies that John McCain has embraced for the last eight years and plans to continue for the next four.”

Wait a minute. Did I miss something here? After the bursting of the tech bubble and the 9/11 attacks, George Bush lowered tax rates across-theboard for individuals and investors. The stock market rallied uninterruptedly for five years. The economy expanded from the end of 2001 to the end of 2007. Are we to really believe the Obama narrative that cutting tax rates is the cause of this downturn? Not the credit shock? Not the Obama-supported government mandate to sell unaffordable homes to low-income people and to pressure Fannie and Freddie to securitize these loans? And not the oil shock, as well?

It was really tax cuts that caused this recession?

That’s the dumbest story ever told.

Wednesday, October 29, 2008

Mac Must Make the Investor Case Now

John McCain is gaining traction on the tax issue as he aggressively makes the case that Obama the Redistributor will take your money and give it to someone else, while he, McCain, will create more economic opportunity by growing the pie for everyone.

Key polls — like Rasmussen, Gallup, Battleground, and IBD — show a narrowing of the race to 2 or 3 percentage points just in recent days. This is in part because Joe the Plumber has crystallized McCain’s campaign message to a pro-growth tax-cut recovery plan that reaches out to investors all across the country. Now the big question is whether McCain will stay on message and keep hammering these points home.

Two days ago in Ohio, McCain argued: “We will cut the capital-gains tax. And we will cut business taxes to help create jobs, and keep American businesses in America.” It’s the first time he referred explicitly to his capital-gains tax cut, which would take the investment rate to 7.5 percent from current law of 15 percent.

Against the backdrop of plunging stocks and deflating home prices, that means asset buyers would keep 92.5 cents of every additional dollar of profit from the purchase of underwater stocks, houses, or any other asset. Current law will let you keep 85 cents on the extra dollar. So McCain’s plan is a 9 percent incentive reward to invest and take risks.

Now contrast that with Obama’s capital-gains tax hike to a 20 percent marginal rate (at least). That means you keep 80 cents of the extra dollar of invested profit instead of today’s rate of 85 cents. In other words, that’s a 6 percent penalty compared with current law.

Adding up McCain’s 9 percent reward and Obama’s 6 percent penalty, we’re talking about a 15 percent swing in the after-tax cost of capital and reward for investment. Stocks have already fallen 40 percent from last October’s peak. So the 15 percent differential between the Obama and McCain plans makes a very big difference to the 100 million investors who comprise nearly two of every three votes in presidential elections.

Additionally, McCain would provide a $15,000 capital-loss tax deduction and would lower the tax rate on retired investors who redeem their 401(k)s or IRAs to a rock-bottom 10 percent. Plus, McCain would drop the corporate tax — a big boon to consumers who actually pay the tax — and would keep income-tax rates at present levels.

Obviously, there’s a very significant difference between the Democratic and Republican plans. If only Mac hammers this home in the final days of the election. Sure, folks have a strong dislike for redistribution. They prefer opportunity. They want to grow the pie larger. And they don’t want left-wing activist Supreme Court judges to take away even more of their economic rights. Hence McCain’s case grows even stronger — if he pounds away and makes it. But yesterday on CNBC John McCain never mentioned capital-gains or investors. That’s not the way to do it.

The latest IBD/TIPP poll shows a 46-46 toss-up among investors. That’s not good. What I’m saying here is that while the redistribution argument is working, it needs to be bolstered by a strong case to investors, who are usually the very base of the GOP.

The opportunity is there for Sen. McCain. But he must have a disciplined investor message in the remaining days.

Key polls — like Rasmussen, Gallup, Battleground, and IBD — show a narrowing of the race to 2 or 3 percentage points just in recent days. This is in part because Joe the Plumber has crystallized McCain’s campaign message to a pro-growth tax-cut recovery plan that reaches out to investors all across the country. Now the big question is whether McCain will stay on message and keep hammering these points home.

Two days ago in Ohio, McCain argued: “We will cut the capital-gains tax. And we will cut business taxes to help create jobs, and keep American businesses in America.” It’s the first time he referred explicitly to his capital-gains tax cut, which would take the investment rate to 7.5 percent from current law of 15 percent.

Against the backdrop of plunging stocks and deflating home prices, that means asset buyers would keep 92.5 cents of every additional dollar of profit from the purchase of underwater stocks, houses, or any other asset. Current law will let you keep 85 cents on the extra dollar. So McCain’s plan is a 9 percent incentive reward to invest and take risks.

Now contrast that with Obama’s capital-gains tax hike to a 20 percent marginal rate (at least). That means you keep 80 cents of the extra dollar of invested profit instead of today’s rate of 85 cents. In other words, that’s a 6 percent penalty compared with current law.

Adding up McCain’s 9 percent reward and Obama’s 6 percent penalty, we’re talking about a 15 percent swing in the after-tax cost of capital and reward for investment. Stocks have already fallen 40 percent from last October’s peak. So the 15 percent differential between the Obama and McCain plans makes a very big difference to the 100 million investors who comprise nearly two of every three votes in presidential elections.

Additionally, McCain would provide a $15,000 capital-loss tax deduction and would lower the tax rate on retired investors who redeem their 401(k)s or IRAs to a rock-bottom 10 percent. Plus, McCain would drop the corporate tax — a big boon to consumers who actually pay the tax — and would keep income-tax rates at present levels.

Obviously, there’s a very significant difference between the Democratic and Republican plans. If only Mac hammers this home in the final days of the election. Sure, folks have a strong dislike for redistribution. They prefer opportunity. They want to grow the pie larger. And they don’t want left-wing activist Supreme Court judges to take away even more of their economic rights. Hence McCain’s case grows even stronger — if he pounds away and makes it. But yesterday on CNBC John McCain never mentioned capital-gains or investors. That’s not the way to do it.

The latest IBD/TIPP poll shows a 46-46 toss-up among investors. That’s not good. What I’m saying here is that while the redistribution argument is working, it needs to be bolstered by a strong case to investors, who are usually the very base of the GOP.

The opportunity is there for Sen. McCain. But he must have a disciplined investor message in the remaining days.

Monday, October 27, 2008

Reagan + Friedman + Keynes

We need all the help we can get

Back in early 1981, when I went to Washington to work for President Reagan, one of the architects of supply-side economics, Columbia University’s Robert Mundell, visited my OMB budget-bureau office inside the White House complex. At the time we were suffering from double-digit inflation, sky-high interest rates, a long economic downturn, and a near 15-year bear market in stocks.

So I asked Prof. Mundell, who later won a Nobel Prize in economics, if President Reagan’s supply-side tax cuts would be sufficient to cure the economy. The professor answered that during periods of crisis, sometimes you have to be a supply-sider (tax rates), sometimes a monetarist (Fed money supply), and sometimes a Keynesian (federal deficits).

I’ve never forgotten that advice. Mundell was saying: Choose the best policies as put forth by the great economic philosophers without being too rigid.

Of course, John Maynard Keynes was a deficit spender during the Depression. Milton Friedman warned of printing too much or too little money. And Mundell, along with Art Laffer, Jack Kemp, and others, revived the importance of reducing high marginal tax rates to reward work, investment, and risk. The idea was to make each of these activities pay more after tax, and in the process boost asset values across-the-board. This incentive model of economic growth was used effectively by President John F. Kennedy and the great 1920s Treasury man, Andrew Mellon.

During the 1980s Reagan enacted Mundell’s three-legged approach. He slashed tax rates on the supply-side and was not afraid to run budget deficits in the Keynesian mold. At the same time, Reagan gave Paul Volcker carte blanche to practice the tough-minded monetarism that curbed excess money and vanquished inflation. This eclectic policy mix reignited economic growth, and it ushered in a three-decade prosperity boom that revived free-market capitalism.

Today, however, the economic naysayers are ignoring the advice of Prof. Mundell. Looking at our financial crisis, with its deflationary sweep from stock markets to home prices to energy, they want to lurch leftward to a big-government tax-and-spend regulatory approach. Instead, we need to put all three legs of the Mundell hypothesis in place. And we’re already two-thirds of the way there.

Treasury man Henry Paulson is using a $700 billion rescue package to prop up banks with new capital, purchase distressed assets, and backstop inter-bank lending. Keynesian deficits will finance it. But it’s working. While ankle biters on the left and right have dissed Paulson’s plan, important credit-market spreads have declined significantly in the last two weeks.

Fed head Ben Bernanke, meanwhile, is combating deflation with a Friedmanite monetarist approach -- the second leg of the Mundell mix. Over the past two months the Fed has doubled its balance sheet and spurred a major increase in the basic money supply in order to meet the enormous liquidity demands that always accompany deflation. The Fed should keep this up in the coming months until stocks, commodities, and credit show life-signs of recovery.

But what’s missing is Mundell’s third policy leg: supply-side tax cuts. And here we find the partisan debate of the closing days of the presidential and congressional elections.

Democrats want to tax the rich, redistribute the wealth, and spend our way out of the economic doldrums. It won’t work. Senators Barack Obama and Harry Reid, along with Speaker Nancy Pelosi, disdain supply-side tax incentives. But Sen. John McCain wants to reemploy them as a recovery tool. McCain is right, and now is the time for the Republican party to call for sweeping tax cuts that would reduce marginal rates by half for businesses, individuals, and investors. Yes, it would be bold. But no bolder than Reagan in the 1980s, Kennedy in the 1960s, or Mellon in the 1920s.

The corporate tax rate should be slashed from 35 percent to less than 25 percent, including capital-gains. (Corporations, let’s not forget, don’t pay taxes. Only individuals do, since business costs are passed along to consumers.) The top individual rate should similarly be lowered, with fewer income brackets to clutter up the tax code. And investment taxes on capital-gains and dividends should be cut from 15 percent to 7.5 percent to revive the dormant animal spirits of investors.

These tax cuts would mean all three legs of Robert Mundell’s pragmatic approach to policy are in place. Use the money supply to combat deflation (inflation is not the problem), employ deficits to rescue and stabilize the banking and credit system, and slash tax rates to reignite economic growth.

In effect, a successful rescue plan requires a drawdown of all the major economic schools of thought. Given the current economic emergency, we need all the help we can get. For a change, how about a little pragmatism in the policy mix? That just might do the trick.

Wednesday, October 22, 2008

Washington to Wall Street

Obama’s Treasury-Ready Men

There’s a huge multi-thousand word article in this mornings Wall Street Journal on Paul Volcker, the former Fed chairman who conquered inflation during the Reagan years and has become a key financial advisor to Sen. Obama. Articles like this fan the flames of speculation that Volcker could be Obama’s secretary of the Treasury, despite his 81-year-old senior citizen status. But Volcker is a vigorous 81 and I think he could handle the job.

Of course, Volcker has a great reputation as a deficit-cutter and a strong-dollar man. What’s more, as a long time financial advisor who was president of the New York Fed, undersecretary of the Treasury, and of course Fed chairman, Volcker’s money knowledge would gain bipartisan support to solve the financial crisis, which will surely spill over into next year. Volcker would attract bipartisan support because of his superb reputation. He is not a supply-sider, nor did he agree with the Reagan tax cuts in the 1980s while he was Fed chairman. But he did work well with the Gipper. Reagan’s supply-side tax cuts along with Volcker’s tight money to slay inflation produced a strong economic recovery and proved all naysayers wrong.

Volcker will unfortunately agree with Obama that the top tax rate can be raised. Not good. But he’s very good on tighter spending and King Dollar. And he does have vast knowledge of the intricacies of world credit markets.

I’m sure the Obama campaign is encouraging the Volcker speculation, since Mr. Volcker brings gravitas and experience to Obama.

The other likely candidate for Treasury under an Obama administration is Lawrence Summers, the proven protégé who was Treasury secretary during Clinton’s last year and before that undersecretary. Summers also would be a strong player, with wide knowledge of our financial problems. He’s also for a stable dollar. And noteworthy is his long-held criticism of Fannie and Freddie. Like Volcker, Summers would agree to lifting the top tax rate; he is no supply-sider. But also like Volcker, he is a moderate-to-conservative Democrat who would be well received by Wall Street and investors.

Are Stocks Ready to Blast Off?

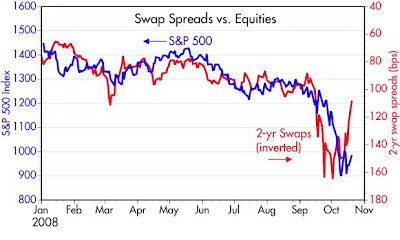

For those like myself who believe the stock market is on the rebound, please go to “Calafia Beach Pundit”, a blog site run by the very smart freemarket supply-sider Scott Grannis. He has a blockbuster chart suggesting a huge rally in stocks.

It’s based on the fact that the two-year swaps spread in the bond market has fallen significantly and is closely related to stocks. His chart suggests the S&P 500 could rebound to 1,200. That would be roughly 20 percent above today’s level.

It’s based on the fact that the two-year swaps spread in the bond market has fallen significantly and is closely related to stocks. His chart suggests the S&P 500 could rebound to 1,200. That would be roughly 20 percent above today’s level.

If Big Mac Wants to Distance Himself from Bush …

The Washington Post reports today that Sen. John McCain is out there on the campaign trail criticizing President Bush in order to deal with the Obama media attack linking Big Mac to W. Apparently McCain is criticizing Bush and Paulson as bailing out the banks rather than buying up underwater mortgages to help homeowners avoid foreclosure.

Okay, fine. I think Paulson’s three-cornered plan to recapitalize banks, buy up toxic assets, and guarantee short-term inter-bank loans in London and New York is the right policy. And since surfacing two weeks ago, the rescue plan is actually helping boost the stock market. But if McCain wants to go there on mortgages, then go there.

However, the senator could distance himself from President Bush in other ways that might resonate with the investor class — the important voting bloc that McCain needs to win by 10 points but is now running even. For example, until very recently the Bush dollar kept sinking. So why doesn’t McCain distance himself from Bush by supporting a King Dollar

that will attract global investment for job creation, hold down inflation, and improve America’s standing around the world? Sen. McCain also could tout across-the-board pro-growth tax reform, such as Paul Ryan’s idea of 10 percent and 25 percent marginal tax rates.

Economic emergencies require strong medicine, and tax reform along with currency reform is consistent with McCain’s message that he will be a real Washington reformer. There’s also McCain’s plan to reform the corporate tax. In this case, McCain’s rate-slashing idea can be sold as a jobs and wages booster and as a tax-cut for ordinary consumers who pay most of

the higher corporate tax that is passed along to them.

These would be very strong economic-recovery ideas that are separate and apart from the Bush policies and have a strong reform message.

There’s a huge multi-thousand word article in this mornings Wall Street Journal on Paul Volcker, the former Fed chairman who conquered inflation during the Reagan years and has become a key financial advisor to Sen. Obama. Articles like this fan the flames of speculation that Volcker could be Obama’s secretary of the Treasury, despite his 81-year-old senior citizen status. But Volcker is a vigorous 81 and I think he could handle the job.

Of course, Volcker has a great reputation as a deficit-cutter and a strong-dollar man. What’s more, as a long time financial advisor who was president of the New York Fed, undersecretary of the Treasury, and of course Fed chairman, Volcker’s money knowledge would gain bipartisan support to solve the financial crisis, which will surely spill over into next year. Volcker would attract bipartisan support because of his superb reputation. He is not a supply-sider, nor did he agree with the Reagan tax cuts in the 1980s while he was Fed chairman. But he did work well with the Gipper. Reagan’s supply-side tax cuts along with Volcker’s tight money to slay inflation produced a strong economic recovery and proved all naysayers wrong.

Volcker will unfortunately agree with Obama that the top tax rate can be raised. Not good. But he’s very good on tighter spending and King Dollar. And he does have vast knowledge of the intricacies of world credit markets.

I’m sure the Obama campaign is encouraging the Volcker speculation, since Mr. Volcker brings gravitas and experience to Obama.

The other likely candidate for Treasury under an Obama administration is Lawrence Summers, the proven protégé who was Treasury secretary during Clinton’s last year and before that undersecretary. Summers also would be a strong player, with wide knowledge of our financial problems. He’s also for a stable dollar. And noteworthy is his long-held criticism of Fannie and Freddie. Like Volcker, Summers would agree to lifting the top tax rate; he is no supply-sider. But also like Volcker, he is a moderate-to-conservative Democrat who would be well received by Wall Street and investors.

Are Stocks Ready to Blast Off?

For those like myself who believe the stock market is on the rebound, please go to “Calafia Beach Pundit”, a blog site run by the very smart freemarket supply-sider Scott Grannis. He has a blockbuster chart suggesting a huge rally in stocks.

It’s based on the fact that the two-year swaps spread in the bond market has fallen significantly and is closely related to stocks. His chart suggests the S&P 500 could rebound to 1,200. That would be roughly 20 percent above today’s level.

It’s based on the fact that the two-year swaps spread in the bond market has fallen significantly and is closely related to stocks. His chart suggests the S&P 500 could rebound to 1,200. That would be roughly 20 percent above today’s level.If Big Mac Wants to Distance Himself from Bush …

The Washington Post reports today that Sen. John McCain is out there on the campaign trail criticizing President Bush in order to deal with the Obama media attack linking Big Mac to W. Apparently McCain is criticizing Bush and Paulson as bailing out the banks rather than buying up underwater mortgages to help homeowners avoid foreclosure.

Okay, fine. I think Paulson’s three-cornered plan to recapitalize banks, buy up toxic assets, and guarantee short-term inter-bank loans in London and New York is the right policy. And since surfacing two weeks ago, the rescue plan is actually helping boost the stock market. But if McCain wants to go there on mortgages, then go there.

However, the senator could distance himself from President Bush in other ways that might resonate with the investor class — the important voting bloc that McCain needs to win by 10 points but is now running even. For example, until very recently the Bush dollar kept sinking. So why doesn’t McCain distance himself from Bush by supporting a King Dollar

that will attract global investment for job creation, hold down inflation, and improve America’s standing around the world? Sen. McCain also could tout across-the-board pro-growth tax reform, such as Paul Ryan’s idea of 10 percent and 25 percent marginal tax rates.

Economic emergencies require strong medicine, and tax reform along with currency reform is consistent with McCain’s message that he will be a real Washington reformer. There’s also McCain’s plan to reform the corporate tax. In this case, McCain’s rate-slashing idea can be sold as a jobs and wages booster and as a tax-cut for ordinary consumers who pay most of

the higher corporate tax that is passed along to them.

These would be very strong economic-recovery ideas that are separate and apart from the Bush policies and have a strong reform message.

Thursday, October 16, 2008

My Interview with Secretary Paulson

Last night, on CNBC's "Kudlow & Company", I had an exclusive interview with Treasury Secretary Hank Paulson. The entire transcript follows:

Kudlow: A very special evening here. The man in the eye of the financial storm. Treasury Secretary Henry Paulson joins me live here in our nation’s capitol. Thank you very much for coming back.

It's a tough day. You know all about that. The market is down over 700 points. Your announcement was yesterday, but we still have the bumpy markets. Fear seems to rule. Volatility seems to rule. A lack of confidence everywhere. Let me ask you, sir. Are markets missing something with respect to your new plan? How do you comment on this, because it just doesn’t seem like there is a wave of confidence.

Paulson: Well, Larry, there's a lot going on right now and a lot going on in the markets. We knew that the financial markets and all the turmoil in the financial markets were going to have a significant impact on the real economy.

Today there was some evidence of that. The retail sales numbers came in at a disappointing level, but not a surprising level. So, I think what the markets are saying today is that they understand that we are going to have a difficult few months ahead of us. But what I would say is let us remember that we have a very resilient economy. Last quarter we grew at 2.8 percent.

The steps we’ve taken are absolutely the right steps. They are bold steps. They are strong steps to stabilize the financial markets and inject confidence into the banking system along with capital. When banks start lending to each other, feel comfortable dealing with each other, they will start lending to businesses and we’ll see this make a big difference in the economy.

Kudlow: Do we have to take a recession? Are we in a recession right now, sir?

Paulson: Well, Larry, what I'm saying is, we're clearly in a difficult period, and it clearly -- the financial turmoil and the very, very difficult time we've had where the credit markets have frozen up, and when loans weren't being made, weren't being made to small businesses, people -- it was hurting jobs, it was hurting confidence, and this has to have an impact. And it's having an impact. But by far the most important thing we can do here is stabilize the markets, stabilize the banking system, and I'm very confident that the moves we've done, taken, will do just that.

Kudlow: All right. I want to get into all those things. They are very important points. Let me begin - front - page stories in all the major papers today. When you unveiled on Monday your rescue package to the nation’s top bankers, apparently it was a somewhat contentious meeting. I want to ask you, first of all, are the major bankers with you? Are they on your team for the rescue package? Second of all, what was the biggest bone of contention in that meeting? What was it you had to sell them on?

Paulson: Well, Larry, let me begin by saying I don’t believe it was a very contentious meeting. I think it was a candid meeting. I think it was pretty extraordinary to get nine bankers running key institutions – institutions with 54 percent of the assets, 50 percent of the deposits in the United States of America -- and to get them to sign up for this plan.

What I said to them was – this is about the United States of America – it's about our economy – it's about our banking system and this is a program for healthy banks. This is not about failure. We want healthy banks to participate in this, because healthy banks need to be well capitalized. They need to be dealing with other healthy banks and with businesses. They need to be deploying their capital. This will be good for the country, it will be good for the system, and good for all of you.

Kudlow: How did you persuade my friend Richard Kovacevich, who runs Wells Fargo? He seems to be the most prominently mentioned. I wasn’t at the meeting and he didn’t talk to me, but from the news accounts, how did you talk him into coming on board?

Paulson: Well, I’ve got to say this. We talked to everyone and there are institutions that could survive just fine without more capital - they have adequate capital - but they need to be well capitalized. What we want to do is to come up with a program. Remember something else about this program. There is nothing punitive about this program. This is a program that said to all the investors that want to come into the banking system, that when the government comes in it is not coming in to squash private investment.

Kudlow: Private shareholders.

Paulson: Private shareholders. No, it is encouraging private shareholders to invest in these banks. So, this is about increasing confidence in the banks and about increasing confidence of the banks and the banking system so that they can be proactive in deploying their capital.

Kudlow: Did some of these bankers worry about management control exercised by the Treasury Department? I mean clearly there are limits to executive compensation. There are limits with respect to dividend payments. And there are generic issues -- will you exercise your warrants and will you exercise voting strength. In other words, is this nationalization? I think that's on the minds of a lot of people.

Paulson: Well anything but. Anything but and this is about taking the preventative action so we don’t need to do any more radical things. Let me just take the issues you mentioned one at a time. These are relatively small positions in ownership terms. These are passive investments. Management -- this is not anything like what you suggested.

In terms of executive compensation, there was broad agreement in that room that this is an important topic. No one spent time debating executive compensation. I explained what the law required and that we were going even further and that there wouldn’t be golden parachutes. If there were profits based upon financial information that turned about to be materially misleading, that compensation would be given back.

Kudlow: Both of which the country seems violently opposed to -- the political nature of the country right now is so much against that kind of thing.

Paulson: And also that we couldn’t have incentives that made compensation based upon excessive risktaking. All of those CEOs in that room understood it. As a matter of fact, when I outlined it, one of the CEOs said "Hank, why are we even spending time talking about this? Of course, we get it."

Again, these are investments that are good for the country and good for the banks. These are temporary investments to bolster confidence and to bring capital to the system. It will be deployed and the economy will pick up and these investments will be refunded.

Kudlow: Do you think that with the preferred stock and all the other aspects you just described -- really, you say passive investments, not active management control -- will that attract private shareholders and private capital, not just the shareholders today, but the potential shareholders tomorrow?

Paulson: Absolutely. I think where people have gotten confused is there have been situations where we’ve had to come in where there is a failure. That is a totally different proposition.

Kudlow: AIG. Fannie and Freddie.

Paulson: Yes -- that's failure. That’s where you have to come in. This is about attracting private capital and it was clear to the whole world that these preferred share investments are going to come in right alongside other senior preferred and not senior to them. And again, preferred doesn't vote with common shares. The warrants are for 50 percent of the value of the preferred shares. And again, the warrants are for non-voting common shares. So, this is about capital and protecting the American people by getting our financial system working the way it's supposed to work. So, we’re going to be able to create jobs. This is about people’s 401k plan. This is about loans to send their children to college and keeping our economy going. That's what it’s about.

Kudlow: So many people want to know. People stop me on the street -- callers on my Saturday radio show -- how can you get the bankers to deploy the government capital that you are injecting? For example, the yield on the preferred is 5 percent. Their cost on the preferred is 5 percent. Some of them have preferred stock that is 11 percent in yield. They have bonds outstanding that are 7, 8, 9, and 10 percent. What is to stop them from getting new government money at 5 percent and retiring the outstanding paper that is much more expensive, rather than deploying this new capital in the economy for the purposes you just described?

Paulson: Well, that's a key question, and let me say, even before that, the reason we set the terms where they were set, we didn't think this term should be set at what the market would demand in a crisis situation. That's why the government's coming in to begin with. We wanted the terms to be like what you would have in a normal situation.

Now, the way you get bankers to deploy the capital -- because they know it's their job to deploy the capital, making the loans which are so vital to our economy -- the way you get them to do that is they've got to have, first of all, plenty of capital; they've got to be well-capitalized. Secondly, they've got to be confident in the system. They've got to be confident that as the money flows between and among banks that they're confident in that and confident in the strength of the system.

Kudlow: Rather than pay down their own debt.

Paulson: They're not going to be paying down their own debt. The regulators understand that and they understand that.

Kudlow: Will you jawbone from time to time -- that's a bad word, jawbone -- will you be talking to them in consultation as you did on Monday, for example?

Paulson: I will clearly be doing that, but I will also say to you that they understand this, and regardless of whether we had government investments there, we would be jawboning and encouraging them to do the right thing. And I will say it will be a lot more effective if people aren’t afraid. This is about confidence and confidence in the financial system.

Kudlow: Mr. Paulson, let me just ask you another question that I hear a lot. People are relieved that you are guaranteeing, the FDIC that is, is guaranteeing the interbank lending. The LIBOR markets are frozen up. Some say the New York markets are frozen up for the short-term loan. That's a huge drag on the whole system. But, let me ask you this – when does this guarantee actually go into place? There is a 75 basis point cost that the banks have to pay. I assume there is some registration. LIBOR rates have slipped a little bit, sir, but not very much. When does this guarantee for the interbank loans really kick in?

Paulson: Larry, I think when you do something as quickly as we rolled this out, there may be some confusion in the marketplace. But, everyone has a guarantee for 30 days. So, there’s a 30-day guarantee.

Kudlow: Immediately?

Paulson: Immediately.

Kudlow: Do people know this key point?

Paulson: They should, because the guarantee is there immediately. At the end of the 30 days they need to subscribe to this. There is a 75 basis point fee. Then, if they subscribe, the guarantee lasts through June of next year. The guarantee applies to the senior obligations coming due -- unsecured obligations -- and they can refund those with a maturity out to three years.

Kudlow: Talking about the freeze up in London and New York and elsewhere, with the benefit of hindsight, was it a mistake to let Lehman go under? Because a lot of people are saying it was precisely the drop off in Lehman, which was roughly in early to middle of September when suddenly LIBOR rates went up, the spread against U.S. Treasuries went up something like 300 basis points and the whole system seemed to go haywire. The whole system was like a computer that completely froze up and there was nothing anyone could do about it. Was the Lehman decision an error?

Paulson: Let me talk a little bit about the Lehman situation. Some of you could argue -- are we dealing with a symptom or are we dealing with a root cause? Because one thing I saw clearly this weekend when we met with central bankers and finance ministers from around the world. There was something very good that came out of that weekend, which was the way in which we all agreed to work together with a common set of policies and objectives. The thing that wasn’t as good was to understand the extent of the problem with financial companies and banks in country after country where they said they didn’t have a real problem, to suddenly then have a significant problem.

But let me get back to Lehman. First of all, Treasury didn't have any powers to do anything as it related to Lehman. We've been very clear. I’ve been very clear when I talked with Congress in July that we didn’t have the authorities to deal with a wind down of a non-bank financial institution. So we were very, very clear about that.

Kudlow: But in truth sir, weren’t you deeply involved in the wind down of Bear Stearns last winter?

Paulson: Yes, working with the Fed and the Fed could loan -- under 13-3 -- they could loan against securities. But there was a hole that needed to be filled in the case of Bear Stearns. There was a buyer, J.P. Morgan. and they could loan against securities.

We worked very hard on Lehman. We all knew about the problem with Lehman for a long time and Lehman tried to work through their problems. I think regulators knew that if there was not a solution before they announced their third quarter earnings, there was apt to be a problem. It turns out there wasn’t a buyer.

There was no hole to fill. There just was not a buyer for Lehman. And, the Federal Reserve didn't think they had the authorities to loan (under 13-3) against Lehman. And I certainly wasn’t urging that because, again, we had a system where we have authorities that were put in place a long time ago for a financial system that existed in a different world and there are broad authorities if a bank fails.

Kudlow: But in truth, when you go back and look at it, the stock market is down 25 percent since Lehman, which was really just a few weeks ago. It was an extraordinary event and, at the time, some people applauded you and said enough is enough we can't take out every bank. But in looking back on it, that seemed to be the trigger to all this recent mayhem.

Paulson: I would say, Larry, looking back there’s a lot that happened. What was going on with Lehman, there is no doubt that when you look at the over-the-counter derivative markets, when you look at the complexity of today's financial world, a failure of any big financial system creates a big issue.

I always look back, in addition to looking forward and deal with the facts presented to us. But I could not have been clearer in June and July, that we didn’t have the authorities. And, we certainly didn’t have them at the Treasury and I don’t believe the Fed had them. If there was a buyer for Lehman -- we had a foreign buyer that was interested -- but near the end their regulator wouldn't let them. So, there was no buyer. There was no hole to fill.

Kudlow: Let’s move on. When you made your statements yesterday regarding the unveiling of the new rescue program, here’s what you said and I will quote. "We regret having to take these actions. Today’s actions are not what we ever wanted to do." What did you mean by that?

Paulson: What I meant was, you know, we're from the United States of America. We believe in free markets. We expect our markets to work well. Government intervention is about failure of a regulatory regime, mistakes on a lot of people's parts, but to me this was much, much better than the alternative. And this was about preserving our free market system and preserving our banking system and stabilizing it for the American people. There’s going to be a good deal of work that needs to be done once we get through this period and a good deal of work to make sure we don’t get like this again.

Kudlow: Some people read your statement and they wondered out loud -- did you mean the changeover in policy from the Treasury purchases of toxic assets to the new capital injections?

Let me read you what you told the Senate Banking Committee -- this is just a couple of weeks old -- in a very difficult Congressional battle, which you eventually won. "There were some that said we should just go and stick capital in the banks. Put preferred stock -- stick capital in the banks. And what to do when you have failures, you know, that what happened in Japan and other spots. But we said the right way to do this is not going around and using guarantees and injecting capital. There have been various proposals to do that, but we want to use market mechanisms."

What was it that made you shift your emphasis away from the toxic asset purchase and towards the injections of capital?

Paulson: Larry, I'm glad you asked me that question. Let me begin by saying that what we were talking about was always capital. Going back over a year ago, I did everything I could to jawbone institutions to raise capital. No CEO ever got in trouble by having too much capital. The illiquid asset purchase is about capital and about price discovery and freeing up capital. We're going to do illiquid asset purchases and it’s going to be integrated very well with the program.

When we worked with Congress we knew we were going to have the ability to purchase preferred stocks if it was necessary. But that statement I made then was about putting in capital if we dealt with a situation like Fannie or Freddie or AIG or we had to move to prop up a failing institution.

Kudlow: But some people are saying that the movement of Europeans toward capital injection, the movement of the British toward capital injection, essentially forced you to play your hand. Is there any truth to that?

Paulson: I look at it differently here. You always need to look at the facts, then the facts before you determine what you do. What we’re doing is very different from what the British are doing. It was clear to me after spending time with the Europeans and what was happening there -- learning more about this situation, that the problem was bigger than we had hoped and that the right way to make a big impact quickly was by purchasing preferreds on the terms of which we did it. That would make the taxpayer money go the furthest. This was clearly an investment where we should get these funds back with a profit.

We moved quickly, but remember let's just talk about what we've done. In just twelve days after the legislation was passed, we had the nine institutions (voluntarily) with 50 percent of their deposits in the United States sign on for a program.

Kudlow: For $125 billion

Paulson: $125 billion

Kudlow: And you’re going to go for a second $125 billion

Paulson: And then we are going to go broadly to other financial institutions and we’ll be going to regional banks and smaller banks and community banks.

Kudlow: That leaves only $100 billion out of the authorization of $350 billion. Is that where the toxic asset purchase comes from?

Paulson: Remember, we have $700 billion.

Kudlow: But you have to go back to Congress for the remainder.

Paulson: For the next $100 billion, all the president has to do is notify. Then, to go beyond that, there is a notification process and Congress has the ability, obviously, to pass legislation to prevent it. In terms of the illiquid assets, this is a $250 billion purchase of preferred equities and it gets very different from what we were talking about when we were talking to Congress. This is a way in which to encourage shareholders to come in and not the way in which I answered the question where we were talking about injecting preferred on a punitive basis.

Kudlow: We talked earlier about the recession or the downturn and the difficult position with retail sales falling three straight months. We really have unprecedented commodity deflation, credit deflation, home deflation, and all the rest of it. When do you think realistically that new credit will flow to consumers, to businesses, to state and local governments? When do you think Americans can realistically expect that to happen?

Paulson: Larry, that is the important question and that, more than anything else, will make a difference in this economy. I've said we have a resilient country and a resilient economy and it can bounce back and this is about confidence. We're going to have a number of difficult months here. We’ve taken the actions that I believe are the right actions based upon the facts that we looked at this week. I think they are the right actions and I think they can make a difference and they can make a difference more quickly than many people recognize, but it’s going to be confidence.

Kudlow: Whoever wins in November -- we’re a few weeks away -- would you be willing to stay on for a few months to keep this process intact before you hand it over.

Paulson: Larry, I’m going to work day and night through January 22 and right after the election I’m available to work with the best transition you’ve ever seen -- with whoever the new Treasury Secretary is. We're out looking right now for permanent leaders of this TARP and we're looking to get someone that will be more than acceptable to the next president and his economic team. This is going to be a first-rate transition -- can guarantee you that.

Kudlow: Mr. Secretary Henry Paulson, we appreciate it ever so much

Kudlow: A very special evening here. The man in the eye of the financial storm. Treasury Secretary Henry Paulson joins me live here in our nation’s capitol. Thank you very much for coming back.

It's a tough day. You know all about that. The market is down over 700 points. Your announcement was yesterday, but we still have the bumpy markets. Fear seems to rule. Volatility seems to rule. A lack of confidence everywhere. Let me ask you, sir. Are markets missing something with respect to your new plan? How do you comment on this, because it just doesn’t seem like there is a wave of confidence.

Paulson: Well, Larry, there's a lot going on right now and a lot going on in the markets. We knew that the financial markets and all the turmoil in the financial markets were going to have a significant impact on the real economy.

Today there was some evidence of that. The retail sales numbers came in at a disappointing level, but not a surprising level. So, I think what the markets are saying today is that they understand that we are going to have a difficult few months ahead of us. But what I would say is let us remember that we have a very resilient economy. Last quarter we grew at 2.8 percent.

The steps we’ve taken are absolutely the right steps. They are bold steps. They are strong steps to stabilize the financial markets and inject confidence into the banking system along with capital. When banks start lending to each other, feel comfortable dealing with each other, they will start lending to businesses and we’ll see this make a big difference in the economy.

Kudlow: Do we have to take a recession? Are we in a recession right now, sir?

Paulson: Well, Larry, what I'm saying is, we're clearly in a difficult period, and it clearly -- the financial turmoil and the very, very difficult time we've had where the credit markets have frozen up, and when loans weren't being made, weren't being made to small businesses, people -- it was hurting jobs, it was hurting confidence, and this has to have an impact. And it's having an impact. But by far the most important thing we can do here is stabilize the markets, stabilize the banking system, and I'm very confident that the moves we've done, taken, will do just that.

Kudlow: All right. I want to get into all those things. They are very important points. Let me begin - front - page stories in all the major papers today. When you unveiled on Monday your rescue package to the nation’s top bankers, apparently it was a somewhat contentious meeting. I want to ask you, first of all, are the major bankers with you? Are they on your team for the rescue package? Second of all, what was the biggest bone of contention in that meeting? What was it you had to sell them on?

Paulson: Well, Larry, let me begin by saying I don’t believe it was a very contentious meeting. I think it was a candid meeting. I think it was pretty extraordinary to get nine bankers running key institutions – institutions with 54 percent of the assets, 50 percent of the deposits in the United States of America -- and to get them to sign up for this plan.

What I said to them was – this is about the United States of America – it's about our economy – it's about our banking system and this is a program for healthy banks. This is not about failure. We want healthy banks to participate in this, because healthy banks need to be well capitalized. They need to be dealing with other healthy banks and with businesses. They need to be deploying their capital. This will be good for the country, it will be good for the system, and good for all of you.

Kudlow: How did you persuade my friend Richard Kovacevich, who runs Wells Fargo? He seems to be the most prominently mentioned. I wasn’t at the meeting and he didn’t talk to me, but from the news accounts, how did you talk him into coming on board?

Paulson: Well, I’ve got to say this. We talked to everyone and there are institutions that could survive just fine without more capital - they have adequate capital - but they need to be well capitalized. What we want to do is to come up with a program. Remember something else about this program. There is nothing punitive about this program. This is a program that said to all the investors that want to come into the banking system, that when the government comes in it is not coming in to squash private investment.

Kudlow: Private shareholders.

Paulson: Private shareholders. No, it is encouraging private shareholders to invest in these banks. So, this is about increasing confidence in the banks and about increasing confidence of the banks and the banking system so that they can be proactive in deploying their capital.

Kudlow: Did some of these bankers worry about management control exercised by the Treasury Department? I mean clearly there are limits to executive compensation. There are limits with respect to dividend payments. And there are generic issues -- will you exercise your warrants and will you exercise voting strength. In other words, is this nationalization? I think that's on the minds of a lot of people.

Paulson: Well anything but. Anything but and this is about taking the preventative action so we don’t need to do any more radical things. Let me just take the issues you mentioned one at a time. These are relatively small positions in ownership terms. These are passive investments. Management -- this is not anything like what you suggested.

In terms of executive compensation, there was broad agreement in that room that this is an important topic. No one spent time debating executive compensation. I explained what the law required and that we were going even further and that there wouldn’t be golden parachutes. If there were profits based upon financial information that turned about to be materially misleading, that compensation would be given back.

Kudlow: Both of which the country seems violently opposed to -- the political nature of the country right now is so much against that kind of thing.

Paulson: And also that we couldn’t have incentives that made compensation based upon excessive risktaking. All of those CEOs in that room understood it. As a matter of fact, when I outlined it, one of the CEOs said "Hank, why are we even spending time talking about this? Of course, we get it."

Again, these are investments that are good for the country and good for the banks. These are temporary investments to bolster confidence and to bring capital to the system. It will be deployed and the economy will pick up and these investments will be refunded.

Kudlow: Do you think that with the preferred stock and all the other aspects you just described -- really, you say passive investments, not active management control -- will that attract private shareholders and private capital, not just the shareholders today, but the potential shareholders tomorrow?

Paulson: Absolutely. I think where people have gotten confused is there have been situations where we’ve had to come in where there is a failure. That is a totally different proposition.

Kudlow: AIG. Fannie and Freddie.

Paulson: Yes -- that's failure. That’s where you have to come in. This is about attracting private capital and it was clear to the whole world that these preferred share investments are going to come in right alongside other senior preferred and not senior to them. And again, preferred doesn't vote with common shares. The warrants are for 50 percent of the value of the preferred shares. And again, the warrants are for non-voting common shares. So, this is about capital and protecting the American people by getting our financial system working the way it's supposed to work. So, we’re going to be able to create jobs. This is about people’s 401k plan. This is about loans to send their children to college and keeping our economy going. That's what it’s about.

Kudlow: So many people want to know. People stop me on the street -- callers on my Saturday radio show -- how can you get the bankers to deploy the government capital that you are injecting? For example, the yield on the preferred is 5 percent. Their cost on the preferred is 5 percent. Some of them have preferred stock that is 11 percent in yield. They have bonds outstanding that are 7, 8, 9, and 10 percent. What is to stop them from getting new government money at 5 percent and retiring the outstanding paper that is much more expensive, rather than deploying this new capital in the economy for the purposes you just described?

Paulson: Well, that's a key question, and let me say, even before that, the reason we set the terms where they were set, we didn't think this term should be set at what the market would demand in a crisis situation. That's why the government's coming in to begin with. We wanted the terms to be like what you would have in a normal situation.

Now, the way you get bankers to deploy the capital -- because they know it's their job to deploy the capital, making the loans which are so vital to our economy -- the way you get them to do that is they've got to have, first of all, plenty of capital; they've got to be well-capitalized. Secondly, they've got to be confident in the system. They've got to be confident that as the money flows between and among banks that they're confident in that and confident in the strength of the system.

Kudlow: Rather than pay down their own debt.

Paulson: They're not going to be paying down their own debt. The regulators understand that and they understand that.

Kudlow: Will you jawbone from time to time -- that's a bad word, jawbone -- will you be talking to them in consultation as you did on Monday, for example?

Paulson: I will clearly be doing that, but I will also say to you that they understand this, and regardless of whether we had government investments there, we would be jawboning and encouraging them to do the right thing. And I will say it will be a lot more effective if people aren’t afraid. This is about confidence and confidence in the financial system.

Kudlow: Mr. Paulson, let me just ask you another question that I hear a lot. People are relieved that you are guaranteeing, the FDIC that is, is guaranteeing the interbank lending. The LIBOR markets are frozen up. Some say the New York markets are frozen up for the short-term loan. That's a huge drag on the whole system. But, let me ask you this – when does this guarantee actually go into place? There is a 75 basis point cost that the banks have to pay. I assume there is some registration. LIBOR rates have slipped a little bit, sir, but not very much. When does this guarantee for the interbank loans really kick in?

Paulson: Larry, I think when you do something as quickly as we rolled this out, there may be some confusion in the marketplace. But, everyone has a guarantee for 30 days. So, there’s a 30-day guarantee.

Kudlow: Immediately?

Paulson: Immediately.

Kudlow: Do people know this key point?

Paulson: They should, because the guarantee is there immediately. At the end of the 30 days they need to subscribe to this. There is a 75 basis point fee. Then, if they subscribe, the guarantee lasts through June of next year. The guarantee applies to the senior obligations coming due -- unsecured obligations -- and they can refund those with a maturity out to three years.

Kudlow: Talking about the freeze up in London and New York and elsewhere, with the benefit of hindsight, was it a mistake to let Lehman go under? Because a lot of people are saying it was precisely the drop off in Lehman, which was roughly in early to middle of September when suddenly LIBOR rates went up, the spread against U.S. Treasuries went up something like 300 basis points and the whole system seemed to go haywire. The whole system was like a computer that completely froze up and there was nothing anyone could do about it. Was the Lehman decision an error?

Paulson: Let me talk a little bit about the Lehman situation. Some of you could argue -- are we dealing with a symptom or are we dealing with a root cause? Because one thing I saw clearly this weekend when we met with central bankers and finance ministers from around the world. There was something very good that came out of that weekend, which was the way in which we all agreed to work together with a common set of policies and objectives. The thing that wasn’t as good was to understand the extent of the problem with financial companies and banks in country after country where they said they didn’t have a real problem, to suddenly then have a significant problem.

But let me get back to Lehman. First of all, Treasury didn't have any powers to do anything as it related to Lehman. We've been very clear. I’ve been very clear when I talked with Congress in July that we didn’t have the authorities to deal with a wind down of a non-bank financial institution. So we were very, very clear about that.

Kudlow: But in truth sir, weren’t you deeply involved in the wind down of Bear Stearns last winter?

Paulson: Yes, working with the Fed and the Fed could loan -- under 13-3 -- they could loan against securities. But there was a hole that needed to be filled in the case of Bear Stearns. There was a buyer, J.P. Morgan. and they could loan against securities.

We worked very hard on Lehman. We all knew about the problem with Lehman for a long time and Lehman tried to work through their problems. I think regulators knew that if there was not a solution before they announced their third quarter earnings, there was apt to be a problem. It turns out there wasn’t a buyer.

There was no hole to fill. There just was not a buyer for Lehman. And, the Federal Reserve didn't think they had the authorities to loan (under 13-3) against Lehman. And I certainly wasn’t urging that because, again, we had a system where we have authorities that were put in place a long time ago for a financial system that existed in a different world and there are broad authorities if a bank fails.

Kudlow: But in truth, when you go back and look at it, the stock market is down 25 percent since Lehman, which was really just a few weeks ago. It was an extraordinary event and, at the time, some people applauded you and said enough is enough we can't take out every bank. But in looking back on it, that seemed to be the trigger to all this recent mayhem.

Paulson: I would say, Larry, looking back there’s a lot that happened. What was going on with Lehman, there is no doubt that when you look at the over-the-counter derivative markets, when you look at the complexity of today's financial world, a failure of any big financial system creates a big issue.

I always look back, in addition to looking forward and deal with the facts presented to us. But I could not have been clearer in June and July, that we didn’t have the authorities. And, we certainly didn’t have them at the Treasury and I don’t believe the Fed had them. If there was a buyer for Lehman -- we had a foreign buyer that was interested -- but near the end their regulator wouldn't let them. So, there was no buyer. There was no hole to fill.

Kudlow: Let’s move on. When you made your statements yesterday regarding the unveiling of the new rescue program, here’s what you said and I will quote. "We regret having to take these actions. Today’s actions are not what we ever wanted to do." What did you mean by that?

Paulson: What I meant was, you know, we're from the United States of America. We believe in free markets. We expect our markets to work well. Government intervention is about failure of a regulatory regime, mistakes on a lot of people's parts, but to me this was much, much better than the alternative. And this was about preserving our free market system and preserving our banking system and stabilizing it for the American people. There’s going to be a good deal of work that needs to be done once we get through this period and a good deal of work to make sure we don’t get like this again.

Kudlow: Some people read your statement and they wondered out loud -- did you mean the changeover in policy from the Treasury purchases of toxic assets to the new capital injections?

Let me read you what you told the Senate Banking Committee -- this is just a couple of weeks old -- in a very difficult Congressional battle, which you eventually won. "There were some that said we should just go and stick capital in the banks. Put preferred stock -- stick capital in the banks. And what to do when you have failures, you know, that what happened in Japan and other spots. But we said the right way to do this is not going around and using guarantees and injecting capital. There have been various proposals to do that, but we want to use market mechanisms."

What was it that made you shift your emphasis away from the toxic asset purchase and towards the injections of capital?

Paulson: Larry, I'm glad you asked me that question. Let me begin by saying that what we were talking about was always capital. Going back over a year ago, I did everything I could to jawbone institutions to raise capital. No CEO ever got in trouble by having too much capital. The illiquid asset purchase is about capital and about price discovery and freeing up capital. We're going to do illiquid asset purchases and it’s going to be integrated very well with the program.

When we worked with Congress we knew we were going to have the ability to purchase preferred stocks if it was necessary. But that statement I made then was about putting in capital if we dealt with a situation like Fannie or Freddie or AIG or we had to move to prop up a failing institution.

Kudlow: But some people are saying that the movement of Europeans toward capital injection, the movement of the British toward capital injection, essentially forced you to play your hand. Is there any truth to that?

Paulson: I look at it differently here. You always need to look at the facts, then the facts before you determine what you do. What we’re doing is very different from what the British are doing. It was clear to me after spending time with the Europeans and what was happening there -- learning more about this situation, that the problem was bigger than we had hoped and that the right way to make a big impact quickly was by purchasing preferreds on the terms of which we did it. That would make the taxpayer money go the furthest. This was clearly an investment where we should get these funds back with a profit.

We moved quickly, but remember let's just talk about what we've done. In just twelve days after the legislation was passed, we had the nine institutions (voluntarily) with 50 percent of their deposits in the United States sign on for a program.

Kudlow: For $125 billion

Paulson: $125 billion

Kudlow: And you’re going to go for a second $125 billion

Paulson: And then we are going to go broadly to other financial institutions and we’ll be going to regional banks and smaller banks and community banks.

Kudlow: That leaves only $100 billion out of the authorization of $350 billion. Is that where the toxic asset purchase comes from?

Paulson: Remember, we have $700 billion.

Kudlow: But you have to go back to Congress for the remainder.

Paulson: For the next $100 billion, all the president has to do is notify. Then, to go beyond that, there is a notification process and Congress has the ability, obviously, to pass legislation to prevent it. In terms of the illiquid assets, this is a $250 billion purchase of preferred equities and it gets very different from what we were talking about when we were talking to Congress. This is a way in which to encourage shareholders to come in and not the way in which I answered the question where we were talking about injecting preferred on a punitive basis.

Kudlow: We talked earlier about the recession or the downturn and the difficult position with retail sales falling three straight months. We really have unprecedented commodity deflation, credit deflation, home deflation, and all the rest of it. When do you think realistically that new credit will flow to consumers, to businesses, to state and local governments? When do you think Americans can realistically expect that to happen?